The state of climate reporting in Australia: A data-driven analysis

Previously, we’ve discussed the context around what's happening regarding mandatory climate reporting and why it's happening.

In this post, sustainability expert Sarah Melville-Maguire talks about the research that RSM conducted last year titled “From sustainability marketing to sustainability accounting” and uncovers the relevant industry-specific insights.

The following is an extract from our recent webinar, you can always watch the full recording here.

Research backstory

RSM has been following the climate reporting requirements since 2022 when the government first started talking about them.

This is quite a big departure from the expectations previously that sustainability reporting is about corporate social responsibility, or even about holistic environment, social and governance reporting.

This is very specifically about climate related risks and disclosing the risks for your company. Even though a lot of companies are out there talking about ESG and reporting on ESG, this is quite different, so we wanted to find out exactly what was happening.

We went and reviewed the sustainability reporting practices of more than 1,500 Australian public and private companies. As far as I'm aware, this is the largest research project of its kind that looks into this. Even though it's not an exhaustive list of every possible reporting company, we feel it's a very reasonable sample size.

How prepared is corporate Australia?

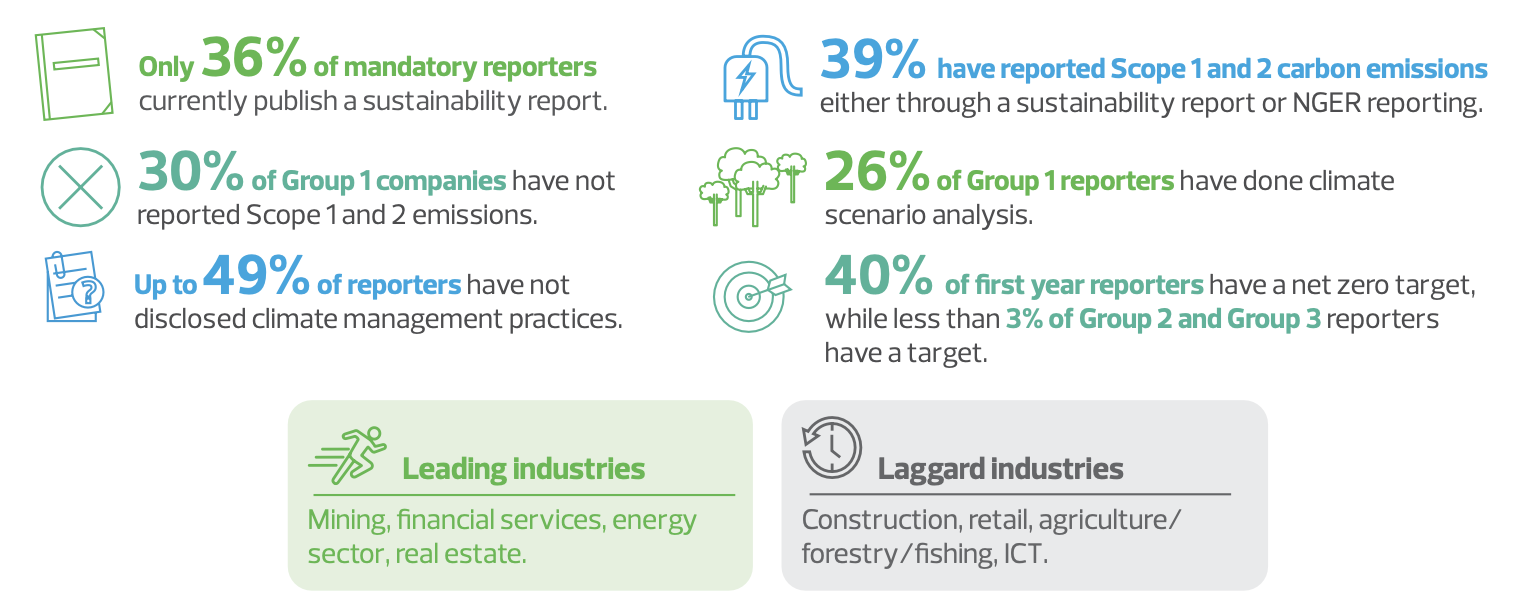

We found that only 36% of companies that would be mandatory reporters are currently publishing a sustainability report, which is really quite low given how advanced sustainability reporting is in Australia.

Interestingly, we found that there are more companies reporting Scope 1 and 2 carbon emissions than they're doing public sustainability reporting. And this is because the National Greenhouse Energy Reporting that occurs. There are many companies required to report their emissions that aren't doing a holistic sustainability report.

We also found, quite alarmingly, that 30% of Group 1 companies have never reported Scope 1 and 2 emissions – albeit that means that 70% are. That's quite a lot of companies that, in just a couple of months’ time, need to be collecting and reporting detailed and auditable information on their emissions that aren't already. So, it's quite a big gap there in that Group 1.

Industry benchmarking

We also looked at a few industry breakdowns and found that there's a couple of industries that are quite far ahead – the mining, financial services, energy sectors were leading industries. And then we found that construction, agriculture, and retail are laggard industries.

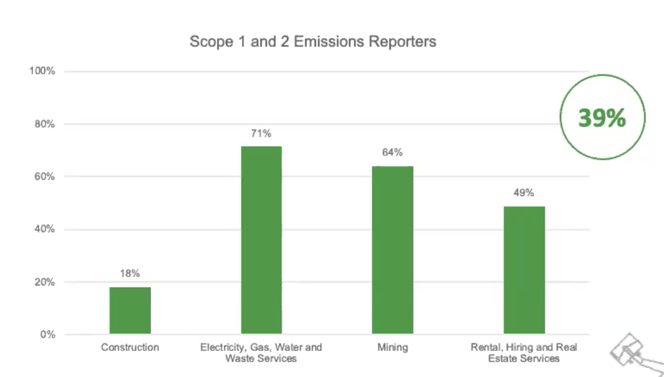

You can see that for Scope 1 and 2 emissions reporters, electricity, utilities and mining are so significantly ahead of the rest of the crowd. We think that this is because a lot of those companies are already publicly listed, and many of them are quite large listed entities on the ASX so they have a lot of external stakeholder pressure in terms of what's expected of their public disclosures. We also see the real estate industry is quite far ahead, which is quite an interesting one.

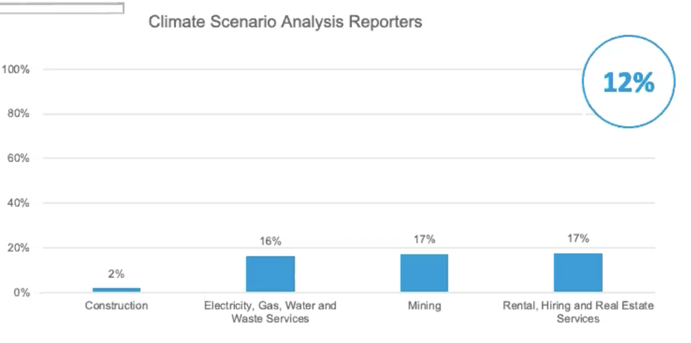

Now, construction's a big laggard in the space of reporting emissions and also in the space of climate scenario analysis.

So, climate scenario analysis is a process whereby which you look at climate models, both from physical impacts and those potential market-based regulatory transition impacts and understand how that can impact your business in the future. It's quite a complex exercise.

But the reason I've shown these two insights is because the Scope 1 and 2 emissions is usually the first thing that companies report. It's not simple, but it is the easiest thing in the kind of breadth of quantitative disclosures that can be made, whereas climate scenario analysis is quite complex - it requires quite a lot of bespoke expertise, not just around your industry and your company, but around climate modelling and understanding climate impacts – so it's usually the last thing that companies will do when they're progressing towards these standards.

And you can see that again, utilities, mining and real estate are slightly above the national average of 12% reporting and construction is quite far behind.

This is something I wanted to talk about: Construction not being as far advanced in these disclosures as other industries. I did mention that the other industries do have a higher rate of being listed entities, but I also think there's some other factors at play here.

In the construction industry, most of the sustainability reporting is related to ISCA, the Infrastructure Sustainability Council of Australia, and they have their own set mechanisms through which they're reporting sustainability.

So, I want to flag that it's not that we think that the construction industry is doing absolutely nothing. It's just that the focus has been on addressing their stakeholder concerns which are usually government-based and fit within a very stringent set of requirements that don't meet the incoming climate reporting requirements.

This is a big shift for every single industry, but I think construction is facing one of the biggest shifts because of that challenge between managing new stakeholder expectations. The construction industry also tends to have a higher rate of private enterprises rather than ASX listed, which again, they just have a different set of expectations around stakeholder communication. So, it's interesting to see that play out in this new context.

-------

Stay tuned for the next part of the series, where Sarah will dive into the nitty-gritty of the four climate reporting pillars, starting with Governance and Strategy.

Or watch the full webinar here.

Recent Articles

Building Brisbane, building the future: Reflections from FCON26

Last week I had the chance to attend FCON26 – the 6th annual Future of Construction Summit – held at the Royal International Convention Centre in Brisbane. Over two days, more than 1,000 construction industry professionals gathered to talk strategy, technology and the future of how Australia delivers.

Why your ERP is costing you more than you think: the case for purpose-built vendor management

Vendor management is mission-critical – so why are so many organisations trying to run it through a system that wasn't built for it?

.jpeg)

How to manage procurement risk across the supplier lifecycle

Procurement risk management is no longer a one-time onboarding task. In asset and capital-intensive industries, supplier risk shifts constantly as vendors move from planning through to delivery and renewal. When procurement is managed across spreadsheets, emails, and disconnected systems, visibility breaks down, data becomes outdated, and risk is harder to manage.

A lifecycle approach allows you to connect vendor onboarding, procurement planning, sourcing, and performance. This way, teams can strengthen their procurement risk management while supporting broader supply chain risk management and third-party risk management objectives.